MANILA, Philippines – With the Tax Reform for Acceleration and Inclusion (TRAIN) bill on its way to becoming a law, income earners can expect additional take-home pay because of lower up-front individual income taxes, but will have to put up with higher prices of transport and cooking fuel, brand-new vehicles and sugar-sweetened beverages, such as soda, among others due to bumped-up other excise taxes.

The joint committee of the Senate and House of Representatives late on Monday, December 11, finished harmonizing the bill in time for prospective ratification within the week, the last session week before Congress goes on Christmas break.

After ratification, the bill will be transmitted to Malacañang for President Duterte’s signature, with authors of the measure hoping it would be ready for implementation by January 2018.

Here are the salient TRAIN provisions in a briefer prepared by Senator Juan Edgardo Angara:

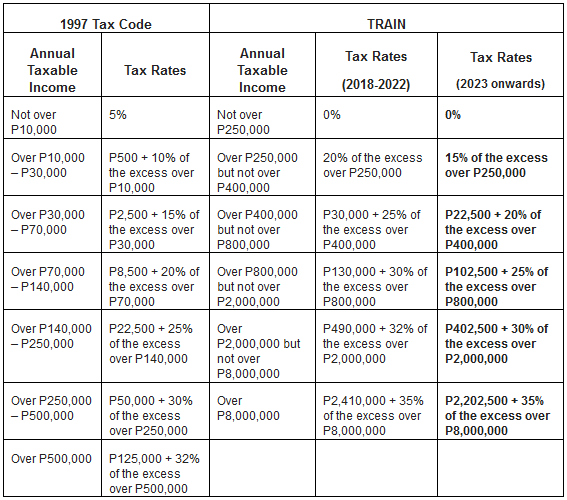

Income Tax

Compensation income earners:

+ Reduced the income tax rates of almost all or 99% of the 7.5 million individual income taxpayers.

+ Exempted the first P250,000 annual taxable income, and raised the tax exemption for 13th month pay and other bonuses to P90,000. This translates to an approximate tax-exempt monthly income of P22,000.

o Based on BIR data, 6.8 million or 90% of the 7.5 million individual income taxpayers will be exempt from paying taxes—more than triple the current 2 million exempt minimum wage earners.

+ Further reduced income tax rates starting 2023.

Self-employed and professionals (SEPs):

+ For easier compliance, introduced the 8% flat tax—in lieu of income tax and percentage tax to be filed once a year—on gross sales or receipts.

o To encourage self-employed and professionals to pay their taxes correctly, which according to BIR data, only contribute 15% of the total income tax collection.

+ The 8% flat tax is made optional for those earning below the VAT threshold of P3 million so they can choose which tax scheme (either 8% flat tax or schedular personal income tax rate with deductions) is more favorable to them.

+ SEPs earning P250,000 and below will be exempt from income tax, and those with gross sales or receipts of P500,000 and below will be exempt from 3% percentage tax.

o Marginal income earners will be exempt from paying taxes just like minimum wage earners. Marginal income earners include farmers and fisherfolk, sari-sari store and carinderia owners, market vendors, tricycle drivers.

+ Filing of VAT and percentage tax returns will be made quarterly. Currently, SEPs should file VAT and percentage tax returns every month.

Petroleum Excise Tax

TRAIN provided for varied increases per petroleum product. For the increase in LPG, diesel and gasoline, the following were approved:

For diesel fuel, for example, from a zero tax rate, consumers will have to pay P2.50 per liter more starting 2018; for 2019, this will increase anew by P2 per liter; and another P1.50 per liter in 2020, or a total of P6 in three years.

Regular and unleaded premium gasoline are being currently taxed P4.35 per liter. This will increase by P2.65 per liter starting 2018, making the tax P7 per liter. By 2019, another P2 per liter will be added, and P1 again for 2020.

As a safeguard provision, the increase would be suspended if Dubai crude oil exceeds $80 per barrel.

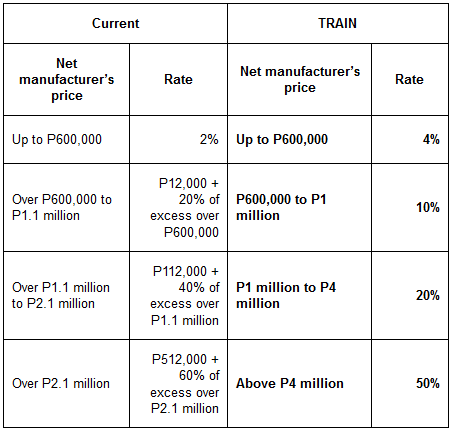

Automobile Excise Tax

The bill provided for a “simpler tax scheme” that is easier to administer. To encourage green and cleaner transportation, electric vehicles will be exempt from the tax, while hybrid cars will be taxed at half the rates. Pick-ups, commonly used by businessmen and entrepreneurs for commercial and agricultural purposes, will also be exempt.

Excise Tax on Cosmetic Procedures

The bill imposed a 5 percent excise tax on invasive cosmetic procedures, surgeries and body enhancements directed solely towards “improving, altering, or enhancing the patient’s appearance and do not meaningfully promote the proper function of the body or prevent or treat illness or disease.”

However, procedures necessary to ameliorate a deformity arising from, or directly related to a congenital or developmental defect or abnormality, a personal injury resulting from an accident or trauma, or disfiguring disease, tumor, virus or infection will not be taxed.

Coal Excise Tax

One of the contentious provisions of the bill, the House and the Senate have agreed to increase the coal excise tax, which has remained unchanged since 1976.

From P10 per metric ton, the new tax will be P50 per metric ton in the first year of implementation; P100 in the second year; and, P150 in the third and succeeding years.

The bill also doubled the excise tax rates of all non-metallic minerals and quarry resources, and all metallic minerals including copper, gold and chromite from the current 2 percent excise tax to 4 percent; and on indigenous petroleum from the current 3 percent to 6 percent.

The excise taxes in metallic and non-metallic minerals and quarry resources were last amended in 1994.

Tobacco Excise Tax

The TRAIN incorporated the bill filed by Senator Manny Pacquiao to increase the tobacco excise tax. The new rates are:

Sweetened Beverage Tax

The bill imposed a tax of P6 per liter for beverages using caloric and non-caloric sweeteners, and P12 per liter for beverages using high fructose corn syrup.

Excluded from the increase are all milk because of their nutritional value (plain milk, infant formula milk, growing up milk; powdered, ready to drink, flavored and fermented milk)

Also excluded are coffee (ground and 3-in-1) being one of the most consumed food items of ordinary Filipinos.

Other excluded beverages are: 100 percent natural fruit and vegetable juices, meal replacement and medically-indicated beverages, sweetened beverages that used coco sugar and stevia.

VAT Base Expansion

To provide tax relief to small businesses and to encourage them to grow and generate more and better jobs, the bill increased the VAT threshold from P1.9 million to P3 million. This exempts small businesses with total annual sales of P3 million and below from paying VAT.

Micro, small, and medium enterprises (MSMEs) represent 98 percent of all registered businesses in the country, according to the bill.

It retained the VAT exemption of raw food/agricultural products, health and education, as well as of senior citizens, PWDs, and cooperatives, and the VAT zero-rating of renewable energy, tourism enterprises and BPOs in special economic zones.

The sale of drugs and medicines prescribed for diabetes, high cholesterol, and hypertension will be VAT-free starting 2019.

It retained the VAT exemption of socialized housing (priced at P450,000 and below) and of low-cost housing amounting to P3 million for the next 3 years so as not to exacerbate the 6-million housing backlog of the country. Starting 2021, socialized housing and mass housing projects that are worth P2 million and below located both in and outside of Metro Manila will continue to enjoy VAT exemption.

According to the bill, leases below P15,000 per month and condominium association dues will be VAT-exempt.

VAT exemption of government-owned and controlled corporations, state universities and colleges, and national government agencies will shift to a form of subsidy through the tax expenditure fund (TEF) under the national budget.

In a statement, Siquijor Representative Ramon Rocamora warned of two “pre-emptive insertions in the bicameral conference committee report that could undermine efforts to raise revenues from tobacco taxes and rationalize fiscal incentives.”

He said health advocates are lobbying for a higher unitary tax rate of P60 per pack, instead of the lower tax rate approved by the bicam.

“This is such a pittance,” Rocamora said.

The other pre-emptive insertion that was not present in the House version but came out in the Senate version, according to Rocamora, was the provision that asserts the VAT zero-rating privilege of enterprises located in special economic zones.

“This privilege is currently being enjoyed by ecozone locators but expressly putting this in a new law pre-empts the Department of Finance’s next set of tax reform proposals that rationalizes fiscal incentives,” he said.

Having a zero-rated privilege on VAT means not just being exempt from paying the value-added tax from one’s production of goods and the rendering of services. One can also claim input VAT credits from the VAT that was paid in producing the good or rendering a service provided that the enterprise is located in special economic zones, he added.

Rocamora said that while zero-rating should actually be enjoyed by enterprises that are fully exporting their output as they pay the VAT when their product reaches its country of destination, a lot of locators actually sell part of their output in the domestic market.

“In effect, government is subsidizing the operations of these locators, devoid of any rational study of whether or not they deserve the subsidy in the first place,” he said.